The start of a new year inspires reflection and goal-setting for many of us. And according to a YouGov poll, saving more money is a top-five resolution that Americans are setting their sights on going into 2026. Not far behind saving more money (21% of respondents) was paying down debts (12%), indicating that financial security is weighing heavily on people’s minds.

Saving money and paying off debt can feel like trying to summit a mountain. When your focus is too fixed on the finishing line, it’s easy to write the whole endeavor off as too complicated, too stressful, or simply not the right time. That’s why so many financial experts favor a baby steps approach.

Can you commit to just 30 days of slashing spending on unnecessary categories? This no-spend challenge is a great way to tackle a savings strategy within a fixed timeframe, gameify it, and demonstrate that yes, it really is doable. Give it a try and see how much you can sock away.

What Is the 30-Day No-Spend Challenge?

The 30-day no-spend challenge is a short-term reset where you pause discretionary spending for a whole month. You will still cover the essentials, but “fun money” is off the table for the time being. Imagine that you’re putting your spending habits on a diet. Grabbing coffees, making quick Amazon orders, or having lunch delivered are all things that quietly drain your budget over time. This challenge exposes just how fast those habits can add up.

How Does the 30-Day No-Spend Challenge Work?

It’s simple: For 30 days, you commit to setting spending rules. Essentials are allowed, non-essentials are not allowed.

What counts as essential or non-essential in your life? The answer will look different for everyone. Rather than try to eliminate every single discretionary expense you can think of, pick a few key categories and start there, so you don’t get overwhelmed. Focus on the behavior, not perfection; it’s alright if you don’t define every single cent.

For example, maybe you can start with takeout as one of your categories — no coffee to-go, no fast food, no meal delivery. Go back to the previous month and tally up how much discretionary income you spent on that category alone.

With those parameters set, you might notice a few things immediately:

- Awareness goes up. You might realize that you spend a lot when you’re bored, stressed, or inconvenienced.

- Small things do count. Those little purchases that felt like they “didn’t count” in the moment do, in fact, add up very quickly.

- You were moving on autopilot. For many people, impulse buys happen with so little resistance that they almost occur without thinking. This leads to major overspending.

Here Are the Rules

Write down your plans in plain language. This will be your guide for the next month as you learn how to stop spending needlessly for 30 days.

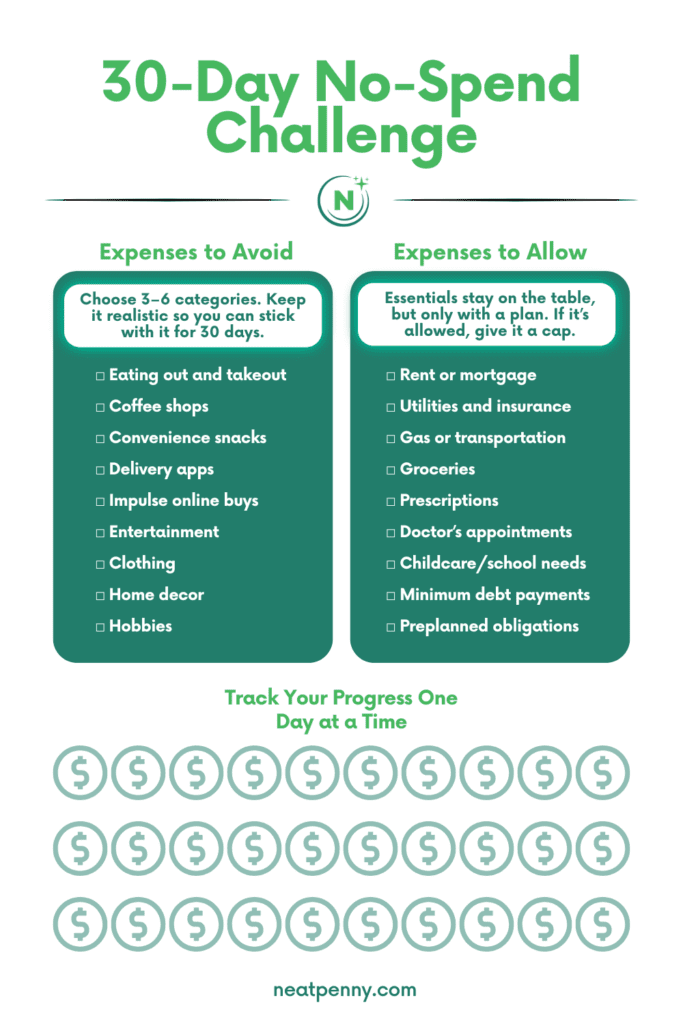

Pick Your No-Spend Categories

Set your off-limits spending categories. You don’t have to choose all of them at once, but some of the most common include:

- Eating out and takeout

- Coffee shops and convenience snacks

- Target runs and browsing other stores “just to look”

- Delivery apps and convenience fees

- Impulse Amazon buys and late-night cart checkouts

- Entertainment: movies, bars, and paid activities

- Clothing, home decor, beauty supplies, and hobbies

Stick with the categories that you know you tend to overspend the most in. This is where you’ll get the most value from the no-spend challenge.

Decide What Spending Is Allowed

The challenge will not include necessary expenses and obligations that can’t realistically be paused for 30 days. Everyone’s list will look different, but common exceptions include:

- Rent or mortgage

- Utilities and insurance

- Gas or public transportation

- Groceries and household basics

- Prescriptions and medical needs

- Childcare and school needs

- Minimum debt payments

- Preplanned obligations you cannot change

The word “allowed” matters here. If it is allowed, it should have a plan for how it will be spent. It is not just a vague pass to spend freely.

Plan Your No-Spend Success Setup

Don’t jump into your no-shopping challenge without a plan to be successful. The prep you do in this stage can determine how successful you are once the challenge actually gets underway.

Start by doing a thorough fridge and pantry sweep. What ingredients are on hand for you to make a simple week of meals? Do this step before every grocery trip to avoid buying more than you need.

Second, create more friction between yourself and your shopping triggers. Unsubscribe from tempting sales emails. Delete saved credit card information from your phone, apps, or browser. Hide or delete shopping apps altogether so you aren’t tempted to browse.

Next, set a dollar amount limit for each of your spending categories, such as a weekly cap for groceries or gas.

If you tend to spend most when you are tired, busy, or stressed out, think about backup plans for those moments. Keep easy meals in the freezer and make a quick list of free activities. Understand that “boring” will be the default for a few weeks.

Build Your Expense Tracker

You don’t need any fancy software or spreadsheets. By simply tracking your progress in your phone, a notebook, or a basic Google Sheet, you’ll see the challenge take shape as real progress. Just note columns for the date, spend or no spend, the full amount, and the category.

For every item that you wanted to buy but didn’t, write that down too; it shows progress. Note what the thing was and what you did instead of spending the money. The “instead” part is really important; it’s the launching pad to building new habits.

Pick Yourself Up When You Fall

Nobody’s perfect. If you have a slip-up, simply log it, note what triggered it, and keep the no-spend challenge going. You haven’t ruined the entire challenge, and there is no need to start over. It’s a learning opportunity to build awareness, simple as that.

Download our free 30-Day, No-Spend Challenge tracker to mark your progress.

Easy No-Spend Swaps to Keep Things Fun

If you’re used to spending money when you’re bored, it can feel really difficult to stay the course. The goal of this challenge is not to remove joy; it’s to learn how to stop paying for it. Try one of these free activities instead:

- Visit your local library, get a library card, and borrow a book for free; you can also use the Libby app to borrow free e-books, audiobooks, and magazines with your valid library card.

- Check your city’s community events page to see if any free local events are happening near you. If your city doesn’t have a calendar page, try local Facebook pages or social media pages for small businesses in the area.

- Challenge yourself to a “use what you have” meal. Cook dinner using only what’s currently available in your fridge and pantry.

- Think outside the box. Crafty hobbies can get expensive, so try to see what you can make only using the supplies you already have on hand.

- Pick a theme or topic — such as “yellow” — and then head out for a walk. Use your smartphone to photograph all scenes related to the topic to make a photo collage documenting your outing.

How to Use the Money You Didn’t Spend

You completed the challenge; now you’ve got some cash saved up! Make your sacrifice worthwhile by putting it to good use. Give your “not spent” money a job.

Pick one plan for the month:

- Debt payoff. Send the extra money to your highest-interest debt. Need a faster, quicker psychological win? Send it to the smallest balance instead.

- Emergency fund. Credit card companies love it when you have an emergency. Don’t give them the satisfaction; pad out your emergency fund and work toward several months’ worth of living expenses.

- Invest it. Managing your own retirement account? It’s time to make another contribution. If you have no investment accounts, now is a great time to open one. Even something small is a good start.

- A specific savings goal. Set the money aside for something specific, like the holidays, a trip, or a car repair.

FAQs About the 30-Day No-Spend Challenge

Can I Still Buy Groceries During a 30-Day No-Spend Challenge?

Yes. Groceries are necessary, so they don’t count against your no-spend challenge. But there’s a caveat: Stick to the essentials. Now isn’t the time to be spending extra on a trendy new snack or fun seasonal items. Make a clear grocery list and stick to it.

If shopping in the store is a trigger for extra spending, see if your grocery store has an online order system where you can shop your list online (or through an app) and then pick it up in-store. Pickup is often significantly cheaper than delivery — some stores even offer it for free.

What if I Need to Buy Someone a Gift?

Try to plan ahead so that your no-spend challenge falls in a 30-day period where there are no birthdays, events, or other special occasions. If this can’t be helped, then it needs to be worked into your “What’s Allowed” category and capped at a set dollar amount. Do not let it derail the whole month.

What Counts as an Emergency During a No-Spend Challenge?

This looks different from household to household, but generally, an emergency constitutes an urgent, necessary, and time-sensitive expense. This could be a medical crisis (for humans or pets), a car breakdown, or a major home repair.

An emergency is not something you want going on sale or restocking.

How Do I Handle a Partner Who Is Not Doing the Challenge?

If you share finances with your partner, it certainly helps to do the challenge together by pausing discretionary spending and putting caps on costs for things like takeout and kids’ activities. If you don’t have full household buy-in, though, you can still track your own personal choices separately to measure progress.

Author

Alicia Taylor

NeatPenny contributor

Alicia Taylor has over 12 years of experience in the editorial space, with a special focus on building financial independence, entrepreneurship, and the FIRE movement. She has worked as a writer and editor for several personal finance publications and aims to help spread the word that personal finance doesn’t have to be intimidating. In addition to writing, Alicia frequently attends financial literacy workshops and conferences, hoping to gain insights that can shape her content to be more informative, actionable, and inspiring.